Adair Turner: Energy Transition Commission

Adair Turner: Energy Transition Commission

Between Decarbonisation and the Devil

Decarb Connect - Adair Turner, Chair of Energy Transition Commission

Lord Adair Turner is the Chair of the Energy Transition Commission (ETC), a coalition of actors from heavy emitting sectors (plus finance) coordinating pathways to decarbonisation. He is also the author of the most cogent book on the financial crisis that I’ve read, Between Debt and the Devil. The ETC’s Keeping 1.5 Degrees Alive report from last September is a great reference document for action to be taken across various sectors from sector decarbonisation, to methane reduction and protecting / enhancing nature (nature being the biggest single ‘sector’ contributing to 2030 goals through ending deforestation and ecosystem restoration). Key Takeaway: Whilst it does feel as though climate action is moving too slowly, there is hope when one looks at the second derivative (the rate-of-change-of-rate-of-change). “Current trajectories” don’t stay current for long.

The ETC was established in 2015 in the run up to Paris with 15 founding members from heavy emitting industries.

Since that time there has been a transformation in acceptance amongst industry about what is necessary, and even inevitable, in terms of decarbonisation, even if the exact path to get there isn’t yet clear in some cases, e.g. shipping

Aluminium: Fairly straightforward to decarbonise as is essentially already an electrolysis process (running electricity through the ore), so that the main challenge is just supplying the zero carbon electricity

Steel: The envisaged path to decarbonising steel has shifted significantly over the last 3 years. Until recently it was viewed that CCS with traditional processes would represent the lion’s share of decarbonisation. However, the industry now sees a much more dominant role for direct reduction, first with methane and then hydrogen [reaction being “Fe2O3 + 3H2 → 2Fe + 3H2O” using hydrogen instead of “Fe2O3 + 3CO → 2Fe + 3CO2”], and a corresponding drop in demand for coking coal by 85-90% by 2050.

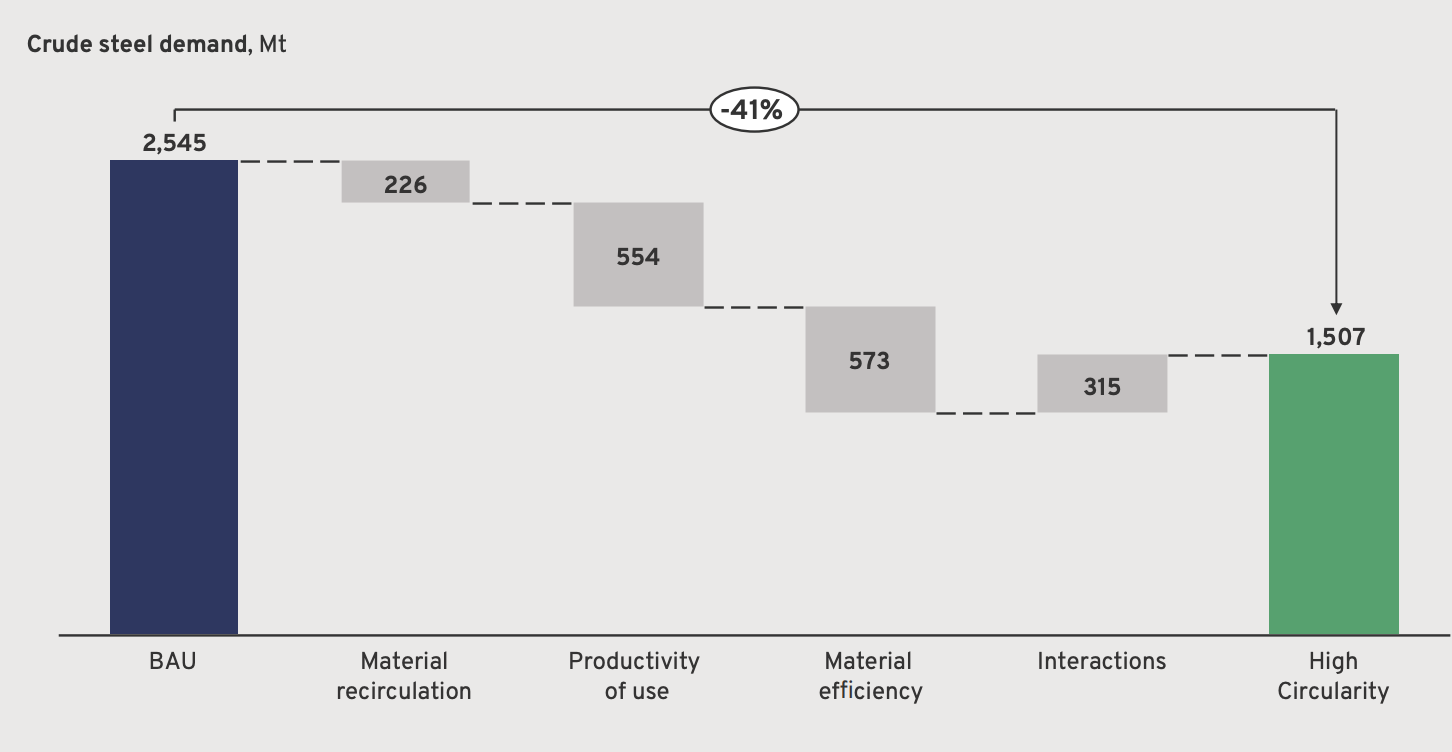

Steel: Full steel sector decarbonisation report available here. Interesting to note that a key element is reducing demand - by 40% by 2050. Also consistent with China’s plan of capping production capacity as part of their decarbonisation plan:

Cement: Decarbonisation will inevitably make cement more expensive than it is today. Need to have sensible ways to pass that cost on. One of the areas that highlights the importance of level playing field in terms of carbon taxes and carbon border adjustments. [CCS relatively straightforward to use with cement production given that the flue gas is a highly concentrated stream and there are technologies being rolled out now that make it even more pure]

Shipping: Probably will go to ammonia or hydrogen, but methanol is also in the mix [This is an interesting take - it strikes me that methanol may steal a march on the alternatives given Maersk’s move there and a number of new e-methanol projects springing up to build the supply chain. The power of procurement is not to be underestimated!]

Finance: There is tremendous momentum to get the finance sector aligned to net zero, but it is very complicated given the myriad relationships between financiers and end emissions. Something like one third of financial assets committed to net zero now through GFANZ and a lot of work being done on implementation.

Lord Turner adds important nuance to the finance question, which is that the important thing for lenders is not just to provide finance to low-carbon industries to reduced the “financed emissions” of their portfolio [a virtue-signalling nonsense which is a particular bugbear of mine], but especially to identify the actors within heavy emitting industries that have a meaningful plan to decarbonise. [The climate transition will be capital intensive so it would be logical to see an uptick in those metrics when banks are financing the roll over to low-carbon infrastructure and business models.]