Implications of rising US power demand

Implications of rising US power demand

Challenges and Opportunities

One of the most interesting themes we’re watching play out is the shift from flat to rising electricity demand in the US and the importance of secure (necessarily), low-carbon (ideally) supply. I have been sitting on this post now for a few months, since the release of the excellent report from Grid Strategies late last year, The Era of Flat Power Demand is Over. The report received some well-deserved attention in the press, so some readers may be familiar with the findings, but there have been a number of related stories more recently that continue to flesh out the shifting dynamics. The key takeaway is this: rising power demand from less climate-sensitive / price-insensitive customers is colliding with the realities of grid constraints to put a fresh impetus on low-carbon firm generation, mostly nuclear. As always, readers’ perspectives and comments are welcome.

Shift in power growth dynamics:

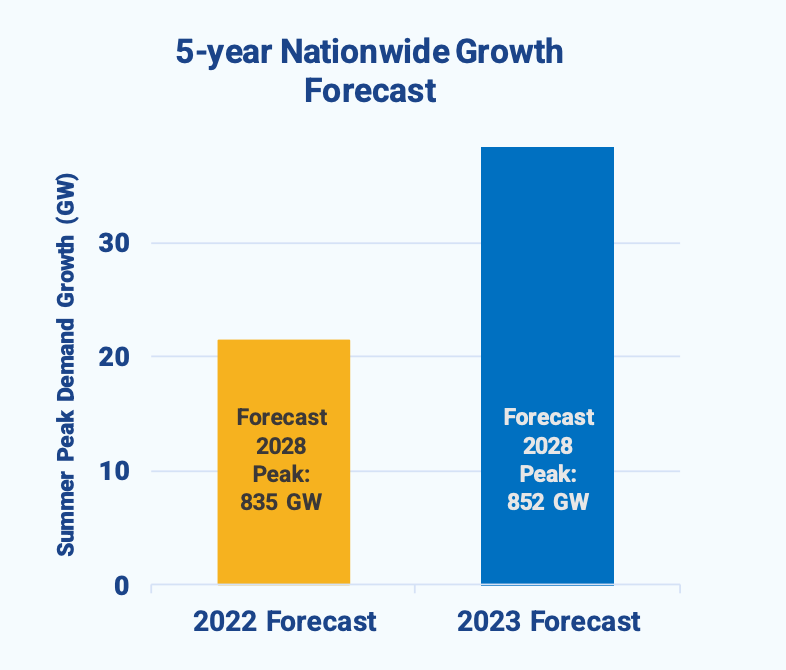

Electricity growth forecasts from utilities nearly doubled between 2022 and 2023, shifting from 0.5% annual growth to 0.9%. Those seem like small numbers, but the result is an additional 37GW peak load in 2028 (around 6x of Ireland’s peak load).

The report notes that this is also likely to be an underestimate. At least four utilities have stated since those forecasts were released that they expect further upward revisions. Also numerous utilities forecast load growth, but haven’t delineated how that translates into peak demand. Lastly, only a small minority of utilities have factored in the impact of hotter average temperatures in summer on demand from air-conditioning. Once that practice is adopted by others, it should contribute to further upward revisions of peak demand.

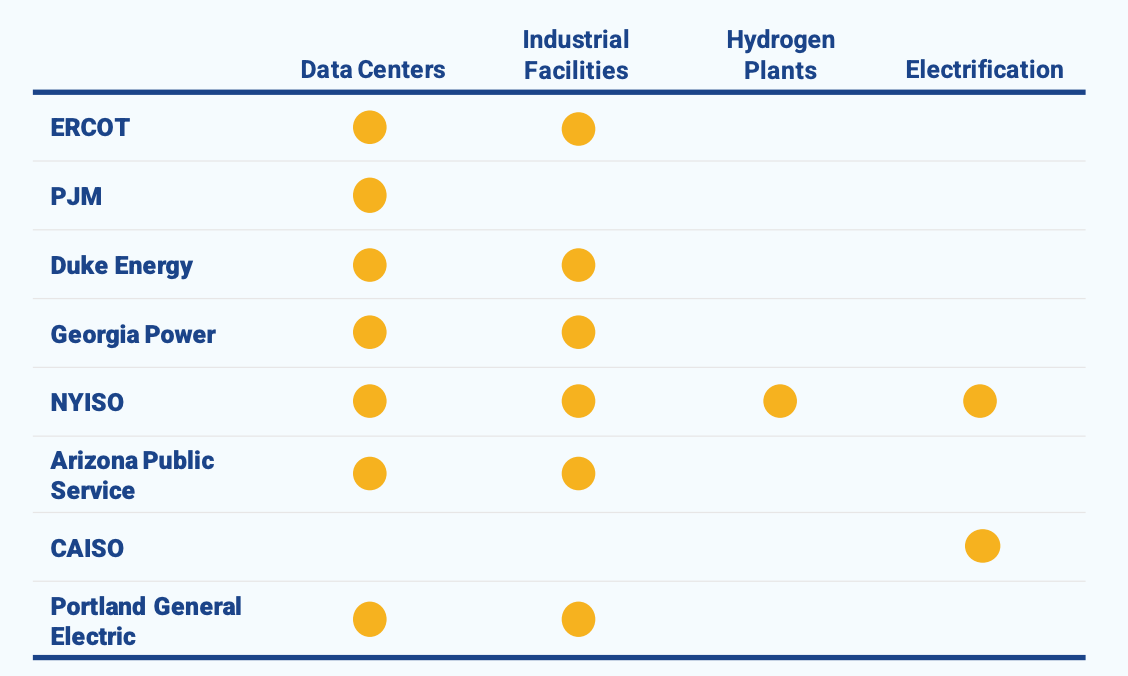

Where is the increase in demand coming from?

It’s not, as you might think, electrification of transport and HVAC. At least not yet, not in most regions (expected to kick in more in the 2030s). The vast majority of the imminent demand growth is being driven by the genuine manufacturing renaissance (batteries and EVs), plus the big tech companies’ huge appetite for power to scale data centres (AI a contributing, but not primary factor). You can see the breakdown of sources of load growth between some of the system operators or utilities here:

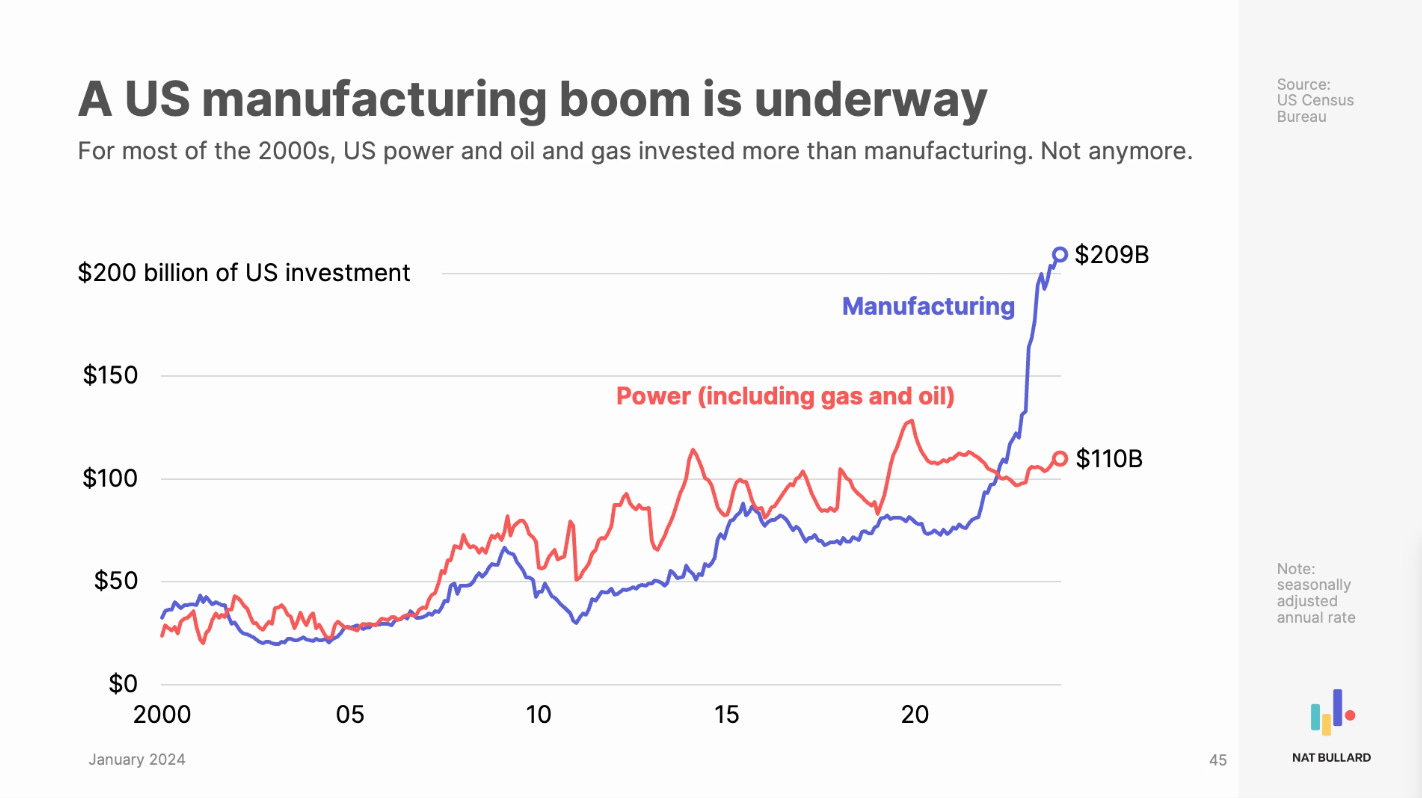

First, manufacturing. Some readers may have spotted the below chart in Nat Bullard’s annual deck:

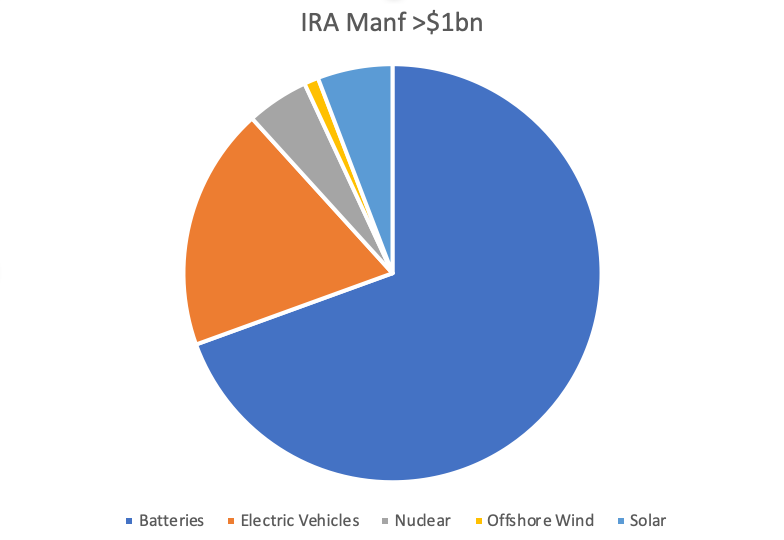

The vast majority of the increase in manufacturing investment is being driven by the IRA. The DoE have an interactive map you can track the investments here. About two thirds of the new investments >$1bn are in battery manufacturing.

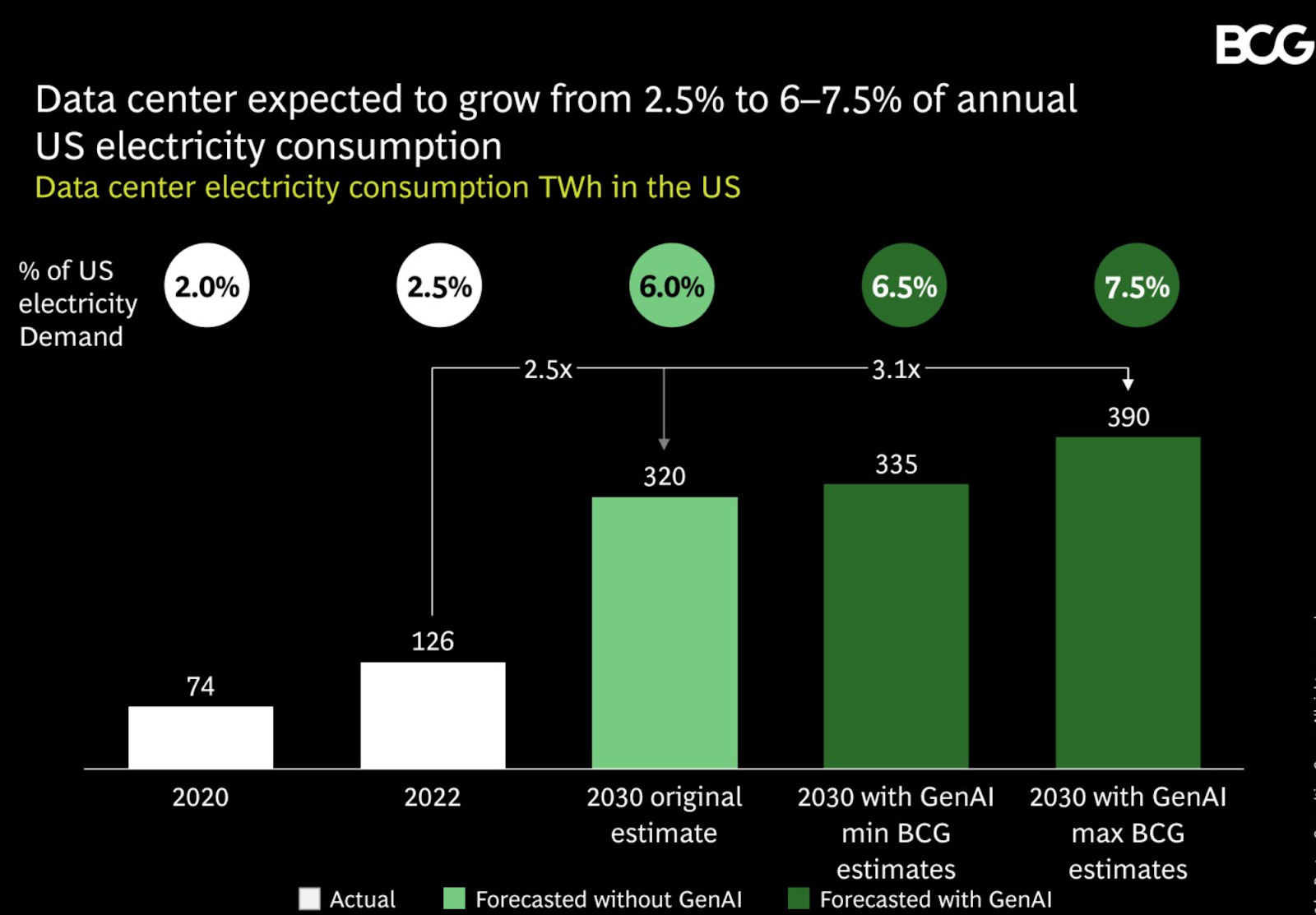

Data-centres: BCG forecasts annual electricity demand from data centres to grow by a whopping 200TWh between now and 2030. To put that in perspective, that’s 6-7x the total electricity consumption of Ireland, my home country. This would see data centre demand grow from about 2.5% to 6-7.5% of US power demand by 2030 (maybe surprisingly given dominance in the press, generative AI only represents a small fraction of forecast increase).

Difference between data centres and industrial facilities - data centres want 99.98% uptime, whereas some of the industrial load can be ramped up and down. In this supply constrained world, we are seeing data centres willing to pay up for new generation sources, so starting to see PPAs for hydro, nuclear and geothermal - more below.

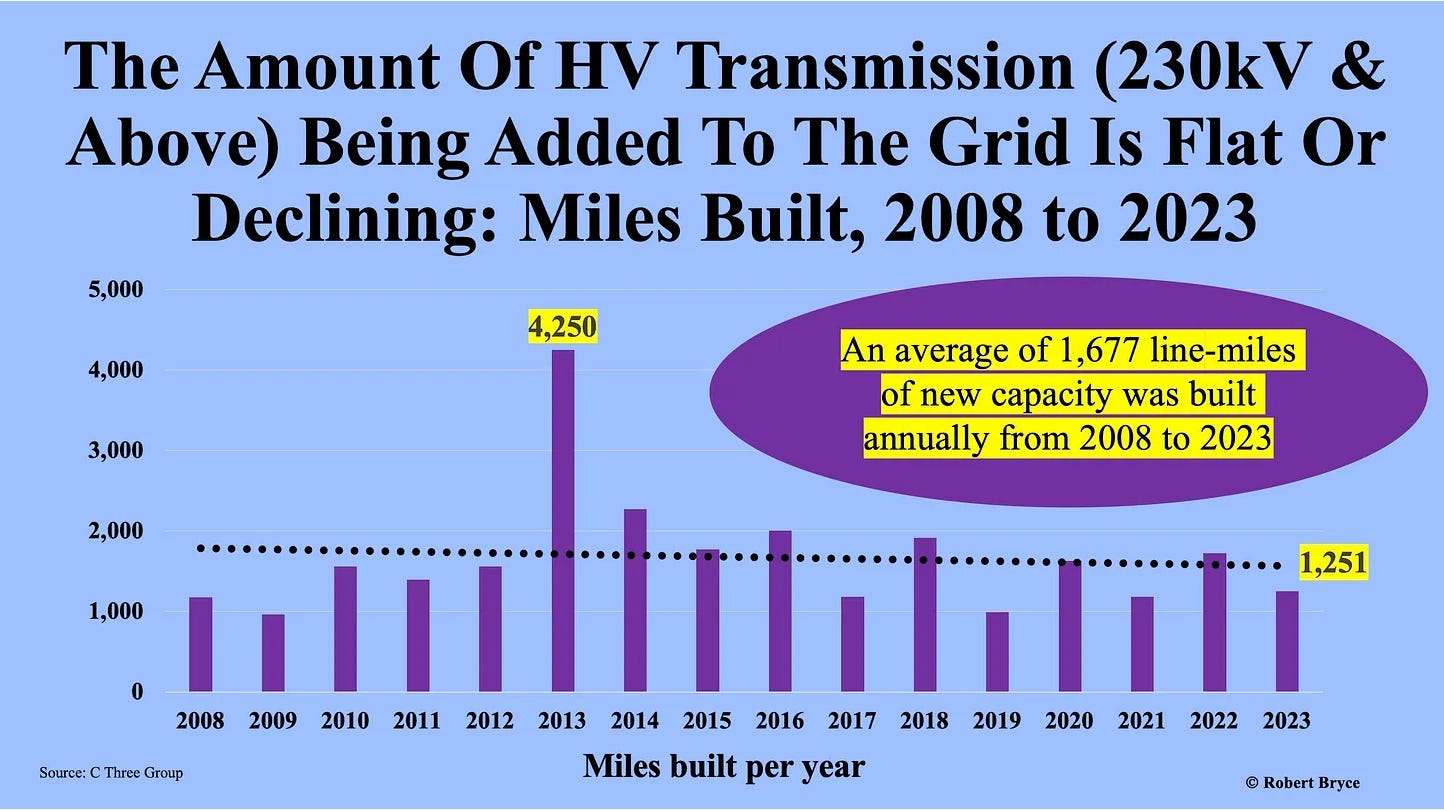

Transmission constraints.

All of this might not be such an issue, if it weren’t for the fact that transmission investment is not keeping pace. According to numbers cited by the GridStrategies report, expansion related investments in transmission have been flat-to-falling at investor-owned-utilities, dropping from $9.2bn in 2021 to $8.8bn in 2023. The US as a whole has been building less transmission over time:

That being said, there is a lot that can be done to get more out of the existing grid. The US only uses 40% of the total grid capacity that is installed on average (not peak). It would be possible to get much, much more out of it with the use of virtual power plants and grid enhancing technologies (dynamic line rating, power-flow control, analytics). The LPO now has billions of dollars of applications from utilities for these types of technologies. Jigar Shah on a recent podcast: “we can unlock 30% more capacity out of the existing grid that we’ve paid for with only a 1% cost of new generators connecting to the grid, that’s how efficient these technology breakthroughs are that we just haven’t deployed at scale yet.”

Hyperscalers paving the way.

All this adds up to a challenging situation, but, like so many challenges, presents a huge opportunity. That opportunity is to rediscover the capacity to do big things. This is absolutely critical if we are to pave a path towards low-carbon energy abundance, which is necessary not only for decarbonisation, but for all the other things we might want to do as a civilisation. As climate-sensitive / price-insensitive buyers of power, the big tech companies have the capacity to catalyse enormous change in the energy system. Some thing that have caught my attention:

Microsoft (the leader of the pack) recently hired Erin Henderson, a veteran of Tennessee Valley Authority, as director of nuclear development acceleration. The company also signed a nuclear PPA with Constellation last year, and contracted with Ontario Power Generation (the utility building the first SMR in the West) for a combination of hydro and nuclear.

Amazon Web Services (AWS) announced this week the acquisition of Talen Energy's data centre campus sited next to Susquehanna 2.5GW nuclear power plant. There are plans in place to develop 960MW of data centres at the site, underpinned by 10y PPAs with the nuclear plant. Story here.

Iron Mountain signed a PPA with Rye Development for hydro capacity added to existing dams.

Google partnered with Fervo Energy on their pilot plant (very small at 3.5MW)

The shift to growing power demand, together with the need to retire more coal power, creates very interesting dynamics for the revival of a domestic (and exporting) nuclear industry in the US, as well as pull-through demand for geothermal. As Jigar Shah noted on that podcast linked above, if you did another reactor exactly the same as Vogtle Unit 4 (conservatively assuming no learnings), and layer in IRA incentives, you’d get to power price of $130MWh. (For comparison, New York recently signed onto $150 MWh PPAs for two offshore wind farms.) Despite all the challenges and overruns experienced at Vogtle, now that they are built, it is much easier for utilities to assess the risk, so some are starting to consider it.

So, in conclusion, US power demand growth:

Presents big challenges to ramp generation, particularly in a transmission-constrained environment

But the emergence of climate-sensitive / price-insensitive buyers, for whom 24/7 availability is critical (hyperscalers) creates a huge opportunity to start to scale up low-carbon firm technologies (nuclear, geothermal, hydro)

Also the constraints should encourage much more rapid deployment of grid enhancing technologies and accelerate reconductoring of existing lines.

Exciting times!

I enjoyed the article and everyone should be aware of the new trend in electricity demand, but I find it puzzling that you do not include natural gas in your list of energy sources that can deal with the new demand.

In North America at least it is the fastest and most cost-effective solution to the problem. New CCGTs are very inexpensive, and natural gas is also very cheap.