Inflation Reduction Act

Inflation Reduction Act

Non-comprehensive commentary

I know what everyone is thinking - if only there was some more content on the IRA! Well, you’re in luck. :-) I’ll resist the temptation to even attempt to summarise the contents of the bill, which was just signed into law yesterday by Biden (for that I’d recommend our friends at Climate Tech VC’s overview). Rather, I’ll just zoom into a couple of aspects that caught my eye in particular. In addition to many articles, I also listened to a few podcasts on this, the best of which was Catalyst’s interview with the excellent Jesse Jenkins of Princeton. The charts below are from his group’s preliminary report, which is very digestible. I’m grateful to all the various parties that have combed the original text and translated it into something comprehensible. Overall, this is a very exciting development, not just for acceleration of decarbonisation, but for its capacity to breath new life into the US industrial base and to support a just transition by focussing on energy communities and with fair wage and apprenticeship requirements. Let’s go!

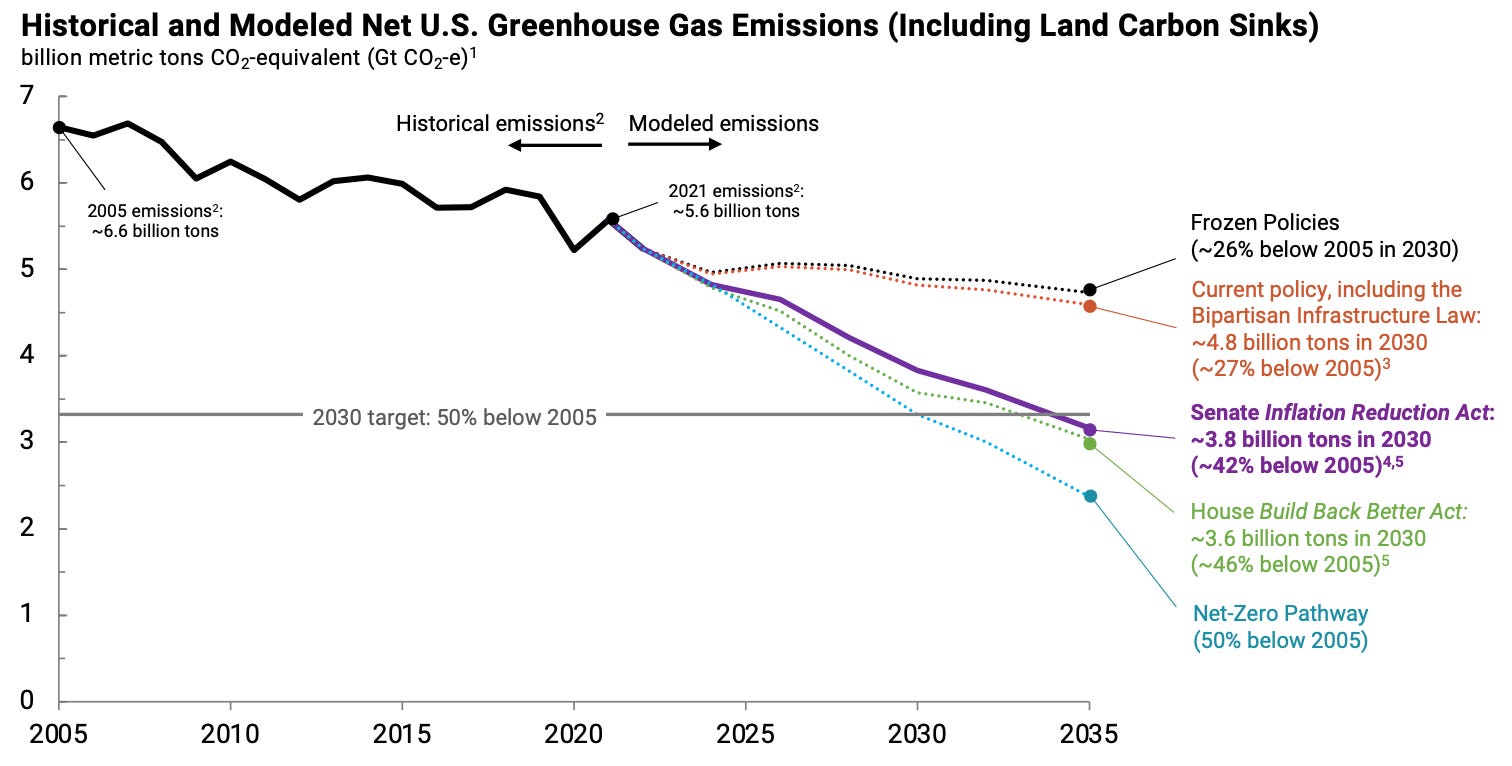

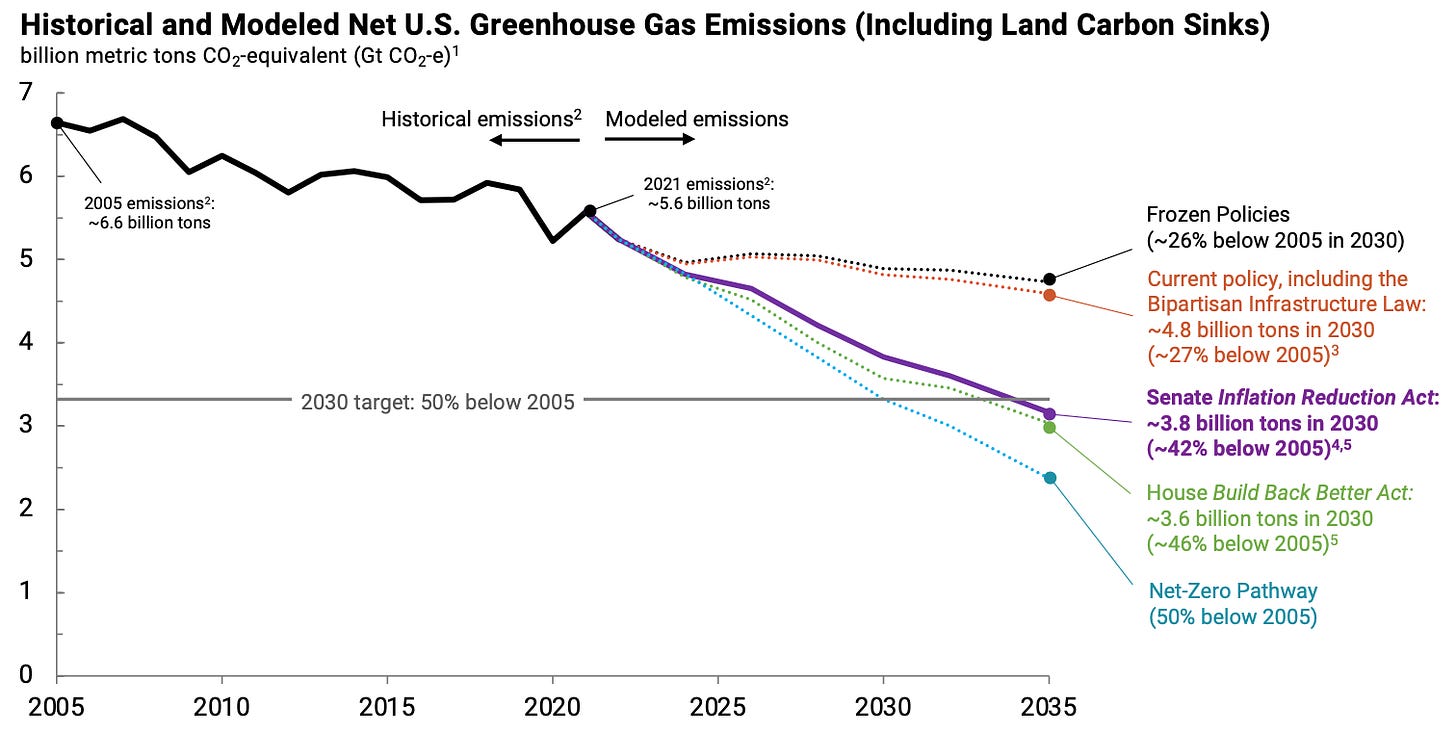

Top line finding - the IRA will cut 2032 emissions by about 1GT vs current policies (2/3 of the gap to the target of 50% cut vs 2005 levels) and will cumulatively trim about 6GT of emissions over the next 10 years.

This leaves a gap of about 0.5GT of annual emissions to get to the 2030 target. However, by reducing the cost of clean technology, the IRA also paves the way for local and state lawmakers to make more ambitious targets.

As the Bill passed by reconciliation (thereby not needing a supermajority in the senate), it has to all be around budgetary mechanisms and therefore is structured mostly around tax credits, although there are also some rebates for low-income households that don’t have much of a tax liability to offset.

You can see from the modelling that, although the IRA was deemed a compromise from the more ambitious Build Back Better Act (which never passed), the difference between the two in terms of modelled emission reductions is minimal.

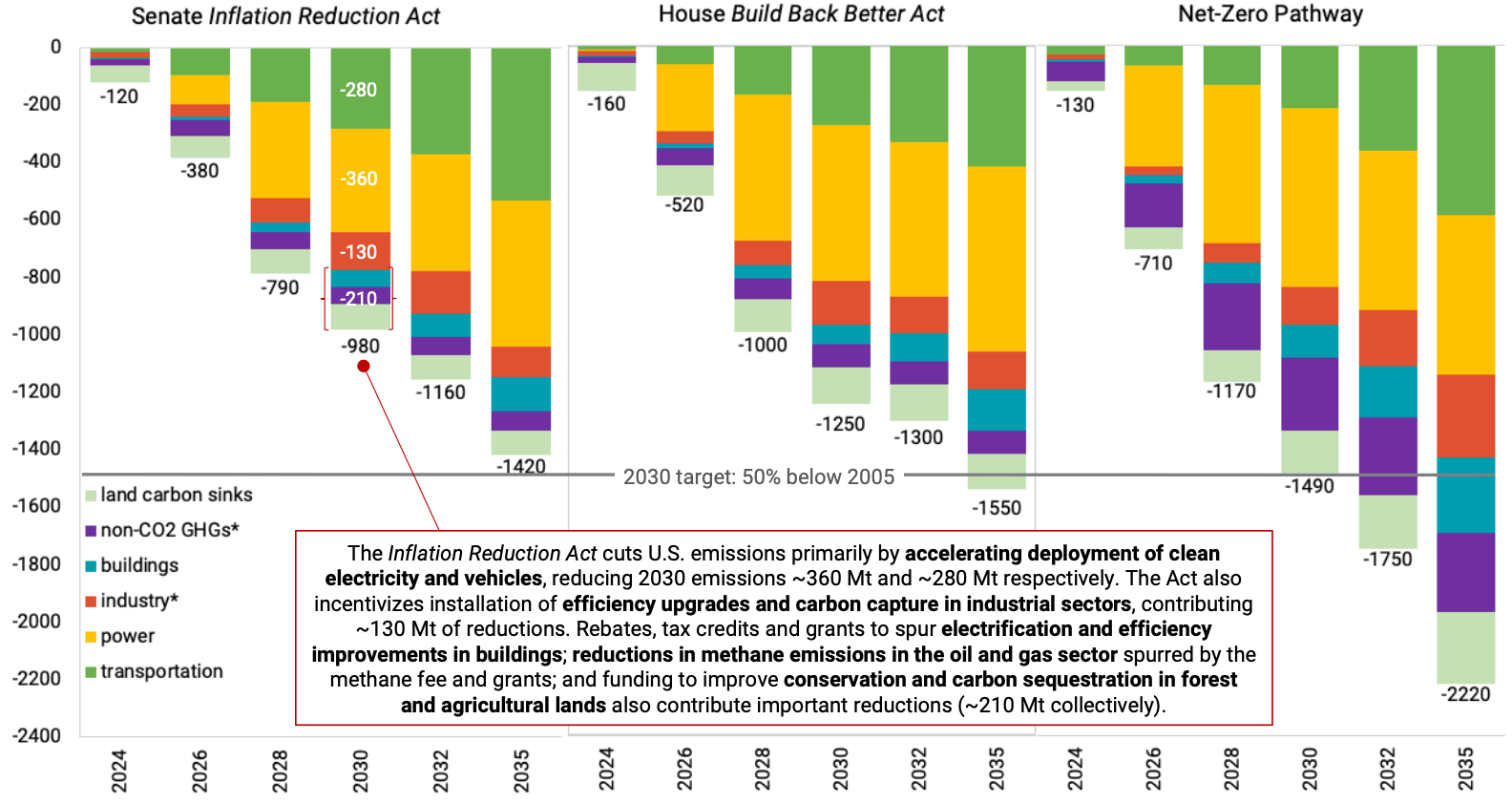

REPEAT Project Accelerating deployment of clean electricity represents the largest emission reductions - something like 360MT annually by 2030. This is primarily achieved through the extension of the production and investment tax credits in clean electricity. Also note that these switch to being technology neutral from 2025, so things like nuclear and geothermal will qualify.

REPEAT Project Annual deployment of wind and solar is expected to increase significantly. Relative to 2020 deployment rates of 15GW of wind and 10GW of utility scale solar, the Princeton team estimate that in 2031 and 2032 – 129GW solar and 31GW wind (i.e. 13x increase in solar deployment). That is modelled taking into account challenges with intermittency, land constraints, etc.

For the accelerated growth of renewables to be realised, there are other, non-financial challenges that need to be addressed, such as siting, permitting, transmission, workforce. However, there is something in this and previous legislation (e.g. Infrastructure Bill) addressing some of these. There is almost $3bn for transmission between construction loans and planning grants in the IRA. And, now that the financial incentives are there, it will increase the constituents that are motivated to get the non-financial bottlenecks addressed.

Further on the roll out of renewables, developers increasingly can negate the grid congestion bottlenecks by using generation for other purposes. This could be for things like electrifying industrial heat (e.g. Rondo Energy or Electrified Thermal) or hydrogen or other. We’ve also seen groups like Intersect Power move in this direction becoming an owner of generation capacity for these off-grid end-uses.

A brief note on transport - it isn’t clear to me how the credit for EV purchases ($7500 for a new EV, $4000 for a second-hand EV - tied to sourcing) are going to accelerate adoption. Demand isn’t the bottleneck at the moment. Quite the opposite - there are significant wait times to get an EV. The brake on adoption seems to be critical mineral and battery supply. These will take time to build out, especially on the mineral side. Happy to understand from any readers how those credits might accelerate real world EV adoption.

Industrial policy. A clear dual purpose of the climate elements of the act, besides decarbonisation, is resilience / self-sufficiency / national security. There are new solar, wind and battery manufacturing tax credits, an extra $20bn for LPO, incentives for retooling manufacturing, expanding domestic critical mineral capacity, and new loan program to address investment in energy communities. Also, there is a bonus credit for domestic sourcing. The government will cover a 10% premium. It isn’t clear if these will accelerate decarbonisation in the US, where stuff might have been sourced from China anyway, but maybe it will add to global manufacturing capacity, accelerating decarbonisation elsewhere.

Energy Communities - there is a 10% investment tax credit for building capacity in energy communities, i.e. areas that are currently economically dependent on fossil fuels or mining. Jesse Jenkins’ group estimates this will support several hundred billion of investments into energy communities. This obviously has Manchin’s fingerprints on it, but is an eminently sensible emphasis. For the energy transition to be successful, it needs to be inclusive, to properly recognise those who might be otherwise left behind by the necessary changes and to make sure that they are not. That is obviously the fair thing, but also practical for reducing political opposition.

Nuclear - tax credits will be available for new nuclear given that the tax credits are for carbon-free power, technology-neutral from 2025. There will also be credits for existing, large-scale nuclear plants that means that it should be economical to keep them all on-line for the next decade. (Note also that Diablo Canyon seems to be on track to have its life extended.) If you stack all of the incentives – 30% investment tax credit, 10% credit for sourcing domestically, 10% for siting in an energy community, you could get a 50% tax credit for new nuclear! This adds fuel to the already popular idea of repowering old coal stations with nuclear. Further, there is $700mm earmarked for the development of domestic HALEU (high-assay low-enriched uranium) supply chain. This is the type of fuel required by many advanced reactors including TerraPower and X-Energy (two recipients of demonstration grants from the DoE). Currently the only place to get HALEU is Russia - not good.

Carbon capture - there were significant increases to the generosity of the 45Q tax credits for carbon capture / removal. The top-shelf credit, for DACS (direct-air-capture w. storage) went from $50 -> $180 per tonne. Boom! (Gonna need a lot of that clean electricity to scale that to any meaningful size.) Interestingly, Jenkins notes in their modelling that the rate limiting factor for CCS/DACS to 2030 will be storage capacity. There is no shortage of geological storage capacity, but a lack of expertise and development capacity (oil companies, behold your future).

Hydrogen – get a $3 / kg production tax credit for very low life-cycle emitting hydrogen, that is through to 2032 – probably too generous given that it makes green hydrogen competitive today the cost is going to come down a lot. The Princeton model shows that demand for hydrogen really explodes in the 2030s and 2040s after the low hanging fruit of electrification.