Energy efficiency and electrification

Energy Transition Distilled: Part 2

Welcome back. In this series of posts I’m trying to boil down the energy transition into its most basic parts and leave readers feeling orientated and equipped with sharper bullshit detectors. In Part 1 (available here), I tried to lay out the picture at the global level with some key concepts. Over the next few posts, I’m going to tackle the main levers for getting from where we are to where we are to where we need to be. I’m tackling these roughly in order of priority, starting from the lowest-hanging fruit, but, in reality, everything needs to happen in parallel insofar as possible. First up, energy efficiency and electrification. Whilst these might be considered two different decarbonisation vectors, they share common ground as the two biggest levers we have for reducing demand for fossil fuels, the biggest contributor to GHG emissions. Even keeping this high-level, there is a lot to cover, so let’s get into it.

We might think of energy efficiency as falling under two broad categories. First, is reducing the amount of useful energy that we require as a society; that is to say, the end amount of energy services we need to achieve our desired standards of living, whether that is in the form of kinetic energy for transport or thermal energy to heat our homes or drive industrial processes. Second, we can think of efficiency in terms of reducing the wasted energy that makes up the gap between primary energy inputs and useful energy services. These two categories work in tandem to reduce the demand for primary energy inputs and, therefore, fossil fuels since they make up 80% of primary energy globally. Because it tends to pay for itself and places less demand on the system, the IEA refers to energy efficiency as the “first fuel” of the energy transition.

No other energy resource can compare with energy efficiency as a solution to the energy affordability, security of supply and climate change crises. - IEA

Electrification meanwhile delivers inherent efficiencies as electrical energy can be converted to useful energy services with low losses, narrowing the gap between final energy demand (the energy that is received by the consumer via whatever form, electricity, liquid fuels, etc) and useful energy. For example, an EV is something like 80% efficient at turning electrical energy into motion, vs around 20% for an ICE turning the chemical energy in petrol into motion. However, the decarbonisation benefit is marginal where the primary energy input is a fossil fuel in the power plant producing the electricity to run the EV, especially if it’s coal.

The real reason that electrification is so crucial to the energy transition is that we have the ability to produce extremely low carbon electricity. By electrifying transport and heating (both buildings and industrial), we effectively expand the addressable market of solar, wind, nuclear, geothermal and hydro.

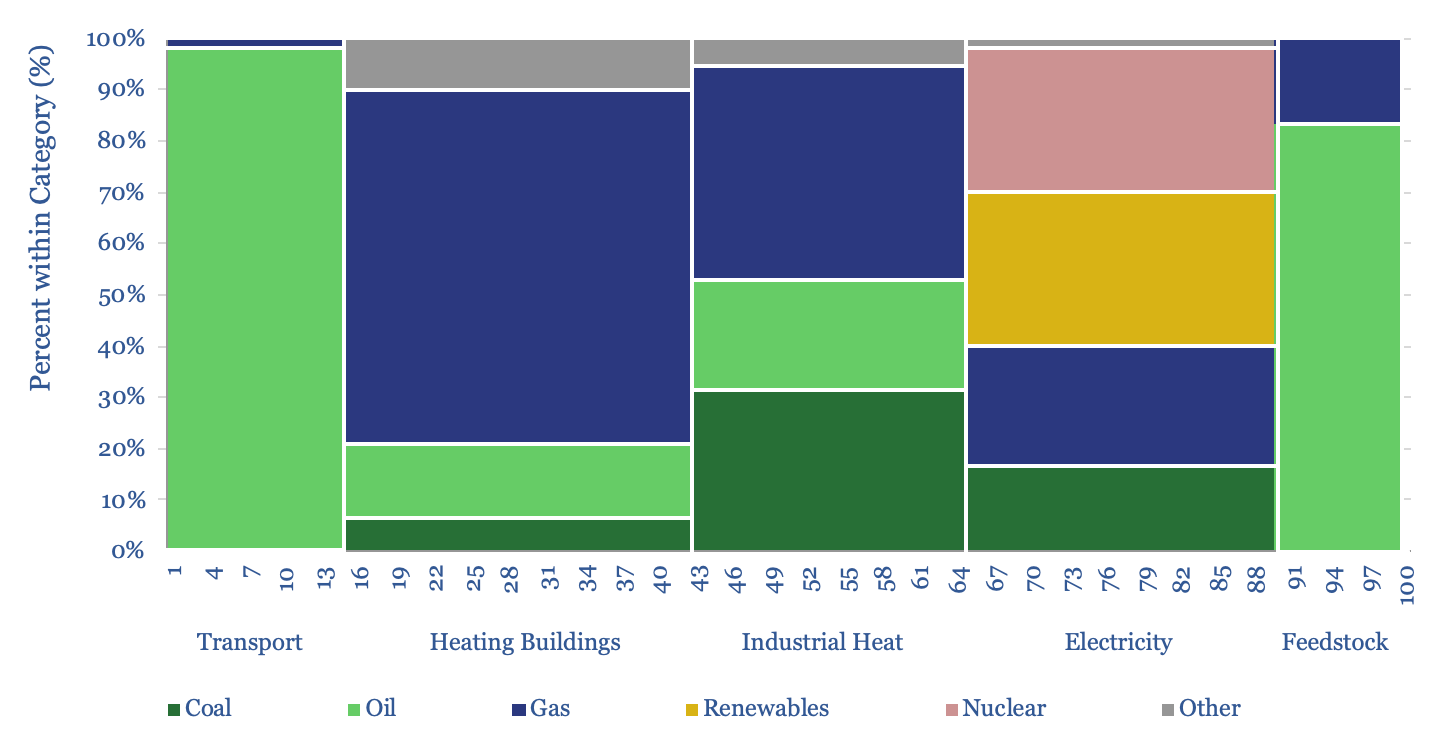

Below is one of the most arresting energy charts I’ve come across. This is (once again) from Thunder Said Energy and shows where Europe gets its energy from, shown as proportions of useful energy.

What is blindingly obvious from this is that the only sector to have any meaningful low-carbon penetration is the electricity sector. By electrifying end uses, we effectively move TWh out of the fossil fuel-heavy columns and into the increasingly low-carbon column of electricity generation.

So what progress is being made within energy efficiency and electrification and what are the main paths available to us to push them forward?

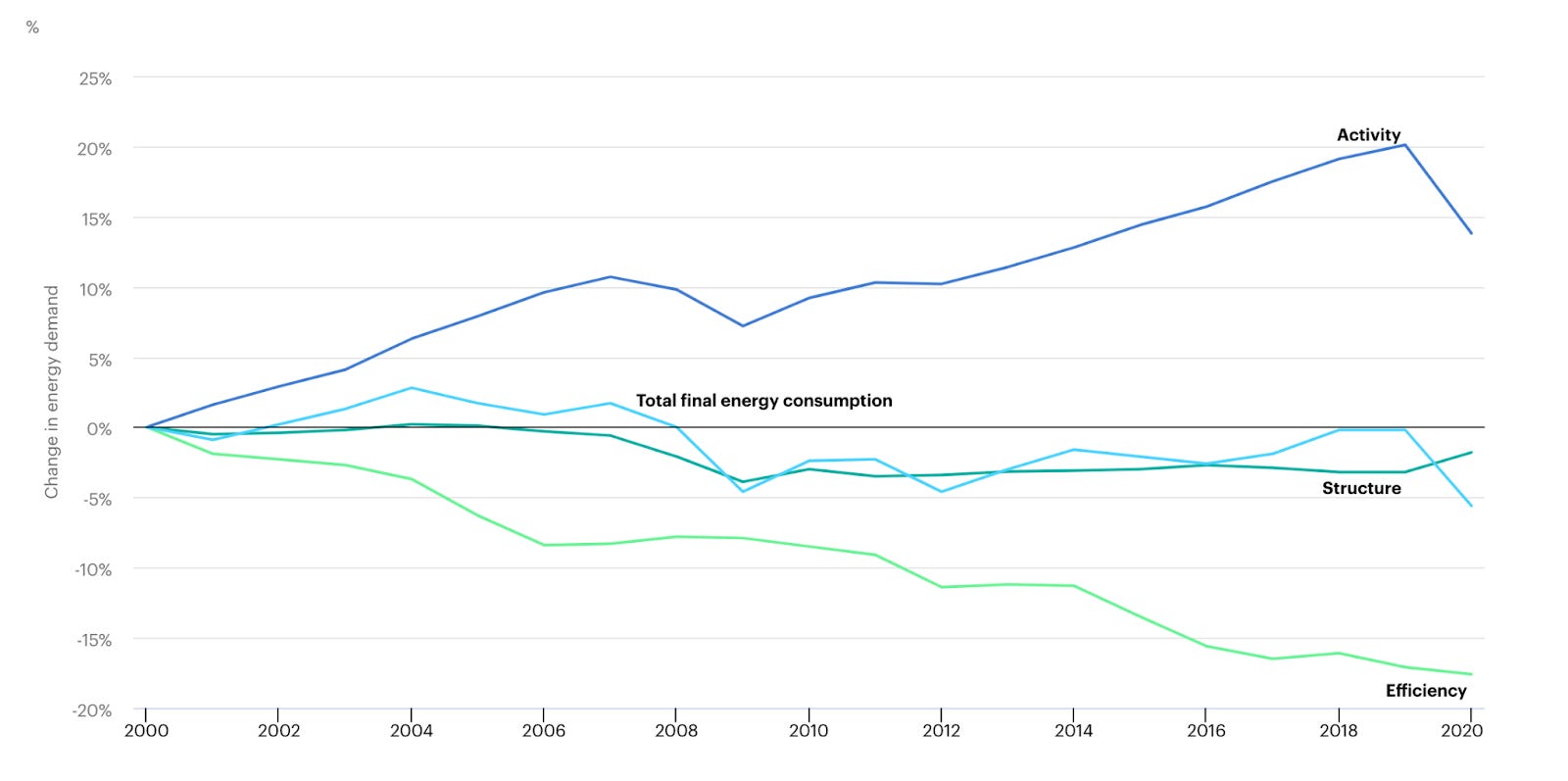

Energy efficiency - the progress: In its latest Energy Efficiency report, the IEA suggests that 4% annual reduction in “energy intensity” (energy / unit of GDP, which you might recognise as the third term in the Kaya Identity from the previous post) is required under its Net Zero scenario. It estimates improvements in energy intensity of 2% this year as a global energy crisis creates urgency, but that progress had slowed almost to a standstill over the pandemic. Still, energy efficiency improvements meant that over the last 20 years final energy demand stayed pretty much flat in IEA countries, which include both developed and developing economies, even as the economies grew 40% in real terms. This is entirely down to energy efficiency as the structure of the group of economies stayed pretty stable, meaning that they didn’t pivot away from energy intensive activities.

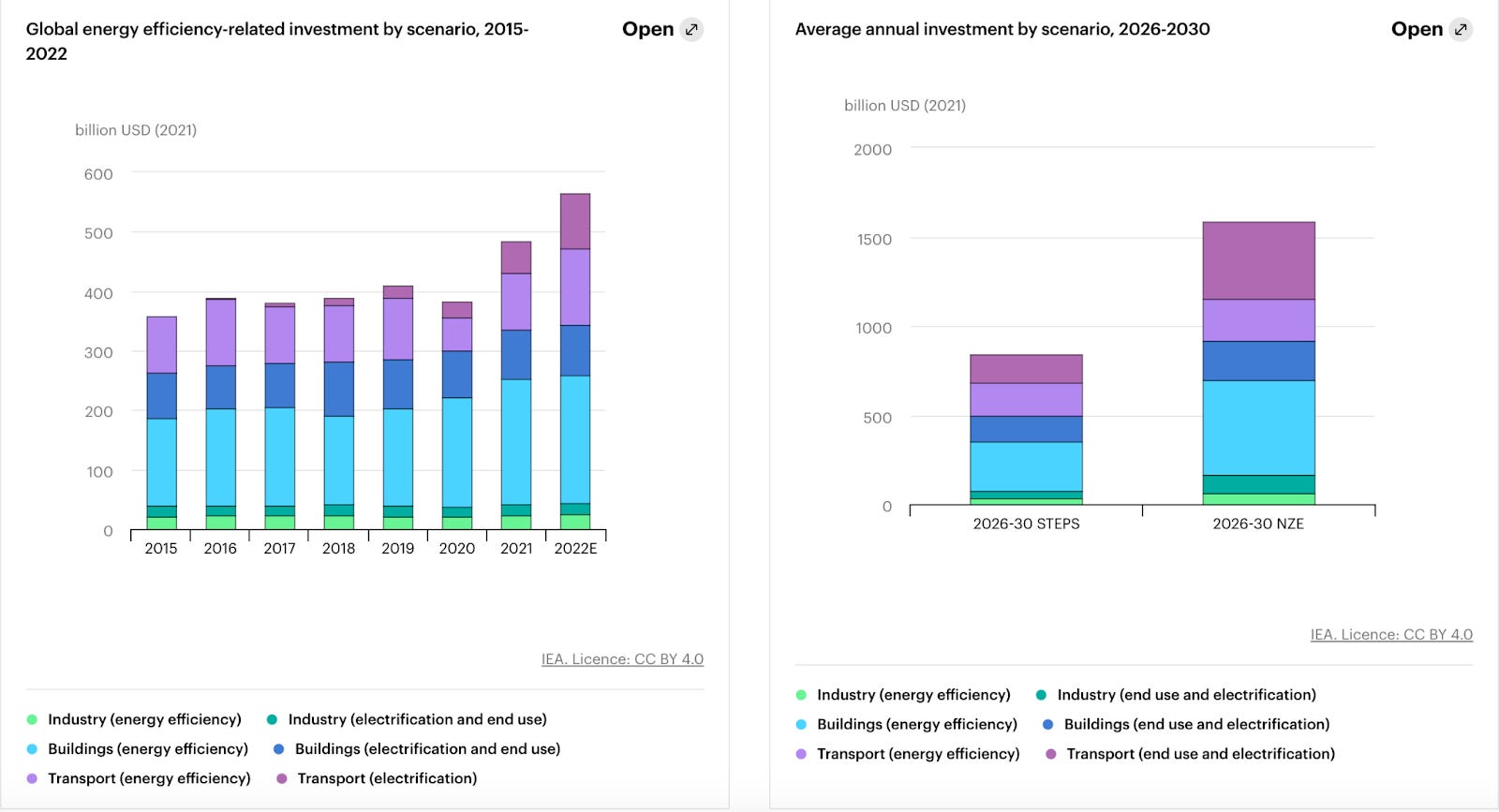

Encouragingly, a lot more capital is being mobilised towards energy efficiency, rising 16% to USD 560bn this year and expected to average USD 840bn in the second half of this decade. However, that is still only half of where it would need to be to get us on a Net Zero path. Note also that the IEA captures both efficiency and electrification in their numbers as both contribute to reduction of final energy intensity.

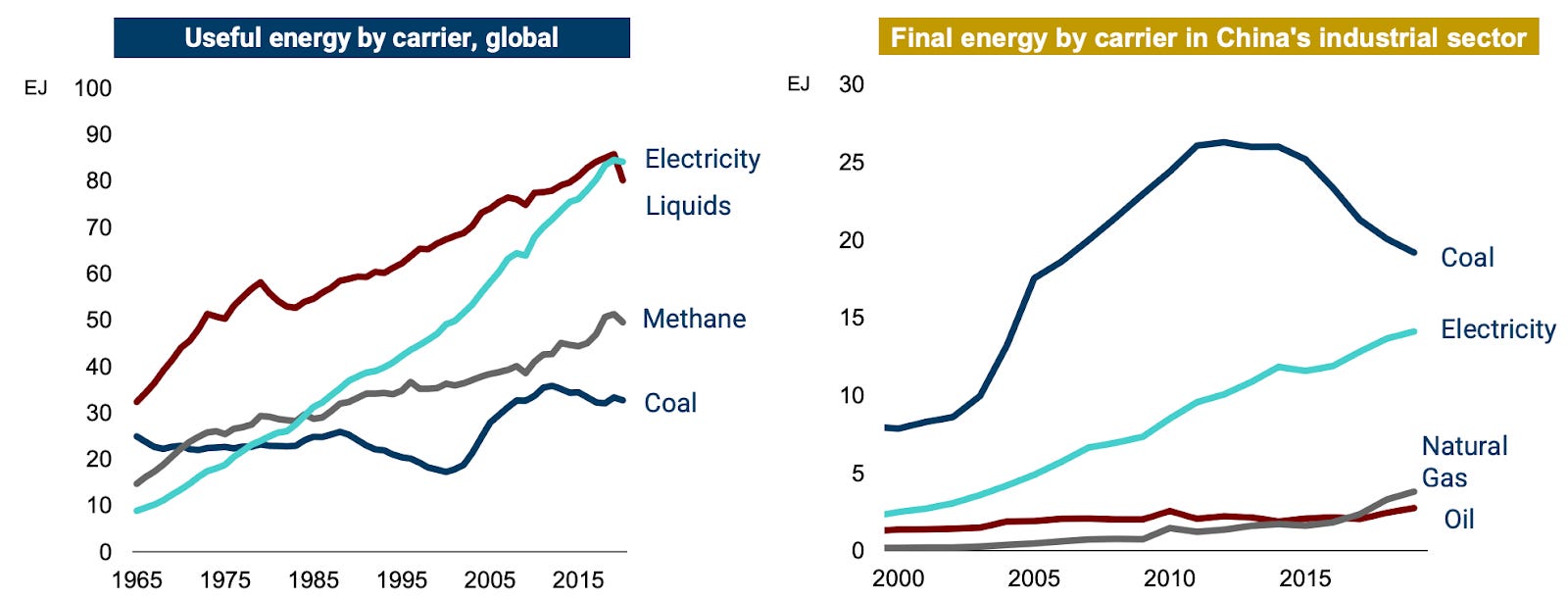

Electrification - the progress: Here, honestly, it is pretty difficult to tell. Most of the data available is on primary energy, which doesn’t tell us that much about the end use. The below charts from RMI’s Energy Transition Narrative document suggests significant progress but it looks more dramatic on a useful energy basis rather than final energy basis (note the numbers on Chinese industrial sector are final not useful - complicated, I know). Also, it seems at odds with numbers from TSE that has electricity’s share roughly stable at 40% of useful energy over the last 30 years.

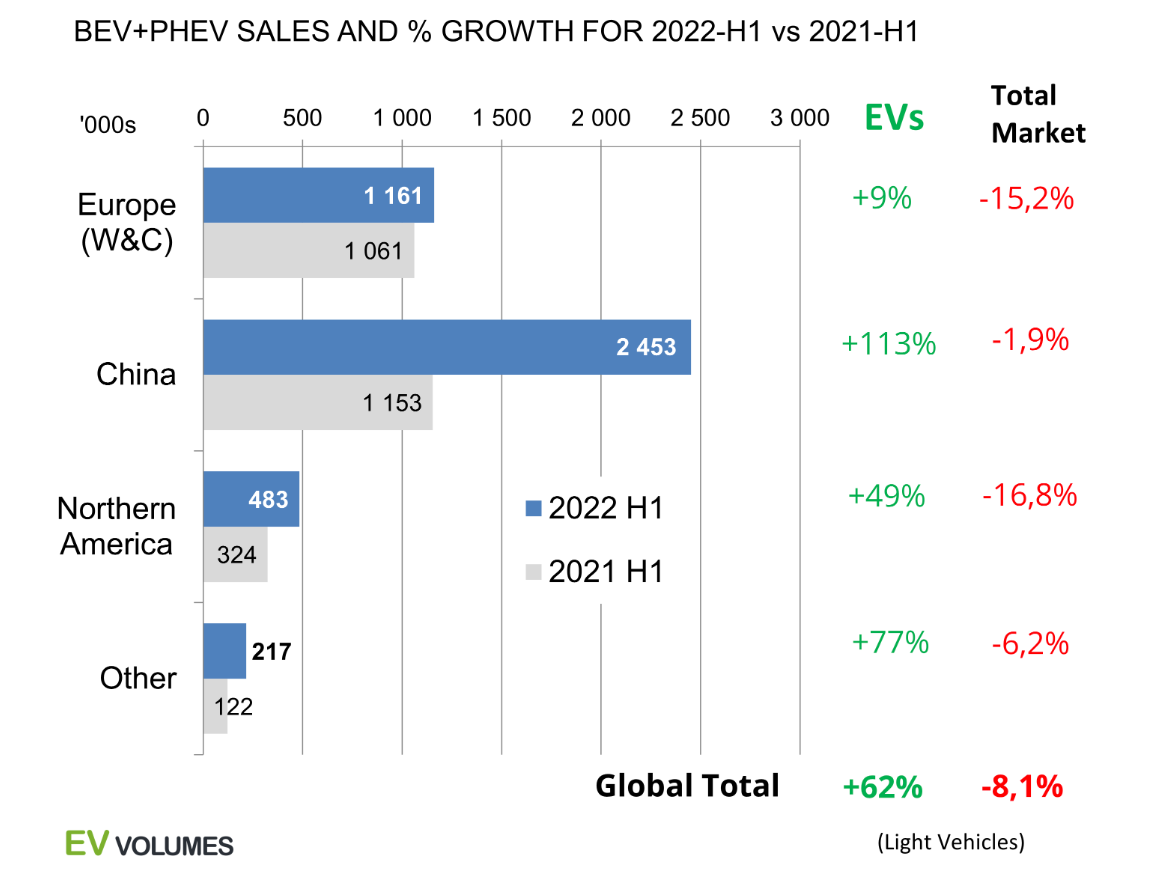

What is indisputable is that we are in the early part of the exponential adoption curve for electrification of some sectors of the economy, most notably light vehicles. I can’t locate numbers for full 2022, but market share continues to increase radically, driven by Europe and China, but with the US looking like it crossed the 5% market share threshold last year. However, this will take a while to filter through to total share of electrification as cars are relatively long lived assets and ICEs still represent 98% of light vehicles globally.

Similarly electrification of space heating via heat pumps is coming from a low-ish base, representing just 9% of global heating demand today. In their recent report on heat pumps, the IEA sees this doubling to 19% by 2030 with very rapid adoption particularly in some European companies looking to get off natural gas. Heat pumps, it should be noted, offer a double whammy of efficiency and electrification. Because they are not turning electricity into heat, but using electricity to pump heat from one place to another by turning a refrigerant back and forth from a liquid to a gas, heat pumps deliver more useful heat energy then they consume in electricity. In normally conditions, residential heat pumps will deliver something like 3-4x the amount of heat as they consume in electricity.

Energy efficiency vectors:

Behaviour change: This is where we all have the ability to contribute and reduces demand for energy services or useful energy. It entails switching from more energy intensive to less energy intensive habits - taking a train instead of a plane, public transport or a bike instead of a car, heating or cooling our homes less aggressively, and consuming less material stuff.

More efficient use of fossil fuels: whilst ultimately the goal is to move away from fossil fuels entirely, improved efficiency in turning primary fossil energy into energy services has delivered massive energy (and carbon) savings while meeting society’s needs. For example, replacing old, inefficient coal plants with modern coal plants was a huge lever in China achieving carbon intensity reduction targets and resulted in a cumulative saving of 1.5GT of CO2 over 10 years. Much more useful energy can be squeezed from fossil fuels by using the heat by-product from electricity production through combined heat and power systems.

Design: A greatly overlooked lever for reducing energy demand as it isn’t a technology per se. Something that cropped up in a podcast with Amory Lovins of RMI that I covered here is that using fatter, straighter pipes and ducts drastically reduces friction and hence the electricity needed to drive the motor. More on integrative design in Lovins’ paper here. Design also contributes towards less material use, including use of steel and concrete in buildings, and lighter, more aerodynamic cars and airplanes.

Building insulation and HVAC (heating, ventilation, air-conditioning): HVAC is the biggest chunk of building energy demand globally at about 40% of the total and responsible for 5GT of CO2 emissions. The amount of energy required is heavily impacted by the envelope of the building (glazing ratio, air-tightness, insulation). In Europe, it takes 3-4x more energy to heat the least efficient homes that the most efficient homes. Then the heating and cooling systems themselves vary wildly in efficiency. Scaling up activity in this area is challenging, but several groups are tackling this through either integrated delivery, financed options or both. Redaptive, focussing on commercial buildings, recently raised an additional $200mm to fuel expansion. Sealed is focussed on residential buildings. Dandelion Energy do ground source heat pumps focussing on the chilly North East US, whilst Woltair again focuses on providing more integrated delivery, operating in European geographies. There is an urgent need for more efficiency in cooling also, given that it represents one of the largest growth areas for electricity demand (3x globally over 30 years) as more people in developing countries can afford it and as the world warms. There are several companies working on more efficient systems, but the biggest lever here is really energy efficiency standards in emerging markets and particularly Asia where the demand growth is coming from (4x over the last 20 years).

Electrification vectors:

Transport: Transport accounts for 30% of final energy demand and is currently almost 100% powered by liquid fuels. The most tractable areas are those that are less energy intensive because of smaller vehicles and operate over shorter distances. The obvious area of progress, as noted earlier, is in light vehicles. EVs are on a clear path to dominate within the next few years. The areas of transport that are deemed eligible for direct electrification have been expanding as battery technology has been improving and costs falling. However, the boundaries will ultimately be constrained by energy density, both “gravimetric density” (energy per unit of mass) and “volumetric density” (energy per unit of volume). For example, jet fuel has a minimum energy density of 42.8 MJ/kg, which compares to about 1 MJ/kg for the best batteries used by Tesla. This puts long-distance flights out of scope for direct electrification, ditto long distance shipping. Hence we will still require molecules for these applications and others, to be covered in a later post.

Heat: Heat represents about half of all final energy use according to the IEA. Of that, it is split roughly evenly between heat use in industry and in buildings. Heat pumps have already cropped up a couple of times here as both an efficiency and electrification vector for decarbonising space and water heating. However, the technology is increasingly able to tackle certain industrial applications that require higher levels of heat. Even for processes that require much higher temperatures, a range of electrification technologies are available from electric boilers to arc furnaces and induction. Work by Dr Silvia Madeddu has found that >90% of industrial heat can be electrified (presentation here and excellent podcast with Michael Liebreich here). I also covered the work of Rondo Energy in a previous post here.

But, of course, for electrification to play its role in the energy transition, it needs to be fed with low-carbon electricity. Supplying enough low-carbon electricity to cover existing uses and all of the expanded requirements through electrification is a daunting task. And that will be the topic of Part 3.